Follow us on LinkedIn

The volatility index was created more than 30 years ago. Since then it has become a favorite tool for both speculation and risk management. There is now strong evidence that VIX futures and related exchange-traded products are changing the market dynamics. Specifically, in the early days of the VIX, the cash market led the futures. But since 2012, VIX futures leads cash 75% of the time.

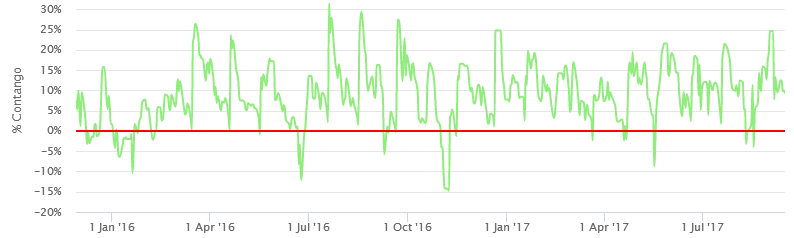

VIX Contango as at Sep 15, 2017. Source: vixcentral.com

Business Insider recently interviewed two of the creators of the volatility index, Robert Whaley and Dan Galai. Here are the key takeaways from R. Whaley interview,

- Where VIX is the volatility over the next 30 days, VIX futures is the expectation of the volatility 30 days from now. Those two series don’t behave like one another, in fact quite differently.

- If you look at VXX and go to 13F filings, you’ll see it’s largely an instrument used by retail customers, not institutions. If you go over to the ownership of XIV, it’s largely institution.

- Retail customers do not look at the prospectus because those things are 300 pages long. Institutional investors do read them and they know exactly what’s going on.

- His investment strategy is to own long term VXX put options and it has worked out well for him. Read more

Regarding bullet point #1, we have repeatedly said that VIX futures are (risk-neutral) expectation values of forward volatilities, and not spot VIX. Furthermore, since they are expection values in the risk-neutral world, they do not represent the future expected value of the spot VIX in the physical measure.

Here are the key takeaways from Dan Galai interview

- It’s hard to say the market is biased one way or another. The VIX is actually reflecting market expectations in the sense that people pay for the options, it’s traded, and anybody can be on any side of the fence. It’s doing its job of reflecting the market consensus going forward.

- The market always has its own dynamics, and the effect is marginal. I don’t think they change the market. Volatility is low, and it’s been low. If the market was expected to change abruptly, we’d see it in options prices.

- When interest rates start moving up, so will volatility.

- There’s no doubt that passive investment and ETFs changed the nature of correlations in the marketplace among different securities. Once you create baskets, you create artificially high correlations between the members of those baskets. Whether it changes the environment in the long term, he’s not sure. We don’t have enough history to make any strong conclusions about it.

- You can find what’s happening in the US on a global basis. You have the same phenomenon of low volatility. Maybe the US is the dominant force, but it’s happening everywhere. Read more

Further questions

What's your question? Ask it in the discussion forum

Have an answer to the questions below? Post it here or in the forum