Follow us on LinkedIn

A common belief among commodity producers, importers and exporters is that hedging should be based on analysts’ expectations. Hence, they often attend meetings where they expect to hear forecasts from analysts and experts. For example, Ed White recently wrote

Meeting halls at farm conferences are packed when the market analysis session is scheduled with farmers eager to hear forecasts on crop prices, livestock prices, fertilizer prices, interest rates and exchange rates.

However, he also pointed out that relying on forecasts for hedging is not a good strategy:

How the heck can farmers hedge loonie exposure when there’s no general consensus on where it’s heading? … currency traders expect to see the loonie in the next year go anywhere from US62 to 89 cents. Read more

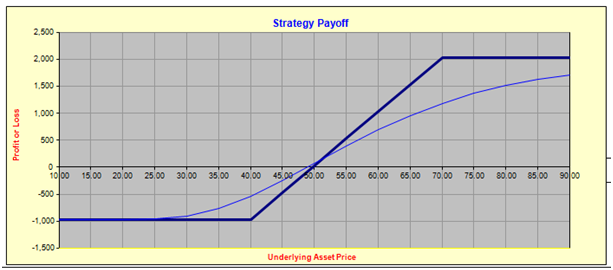

Strategy payoff of a zero-cost collar

Indeed, the job of a corporate treasurer is to identify the relevant risks and find an effective way to hedge them and not to speculate based on his/her own or some analysts’ forecasts.

This point is stressed again by Mark O’Toole

Bracing for uncertainty requires having an accurate view of all your exposures across all asset classes and the ability to stress test what would happen amid the likelihood of certain events. Only then can a company set hedging strategies and determine how events will impact their supply chains.

In the near future, the risks that we are facing are

- The impact of Chinese economy

- Foreign Exchange risks

- The move from IAS 39 to IFRS 9

To hedge against those risks and to ensure a stable revenue, corporate treasurers can carry out hedges using derivative instruments such as fixed price swaps, fixed price swaptions, two-way collars, three-way collars, and basis contracts.

The design of such a hedging strategy would involve: pricing of the derivative instruments, stress testing, and evaluation of the effectiveness the hedge.

Further questions

What's your question? Ask it in the discussion forum

Have an answer to the questions below? Post it here or in the forum